5 Bad Spending Habits You Need to Quit Right Now

Spending money is something we cannot avoid, be it for the necessities in life or for simple pleasures. Nothing comes for free, after all. However, how you spend your money is important as it directly impacts your financial health and could help you reach your financial goals.

When you develop healthy spending habits, you may find yourself with more disposable income that could be put to better use such as setting up emergency funds or saving up for a new home. These small changes can help you realise your financial goals.

Once you recognize your own spending habits, it is time to identify ways to break those bad ones and create healthy ones. Here are five bad spending habits that you may or may not have and how you can change them.

- Daily Coffee

If you need your morning coffee in order to kickstart your day, buying coffee daily might cause a strain on your budget. A coffee from a cafe can set you back at around $5.20 for an Americano, though a more budget-friendly alternative is getting kopi-o from a coffeeshop at a price of around $1.20<.

You don't have to give up on coffee completely to save more money. There are other alternatives to get your daily caffeine boost.

For starters, you can prepare your own coffee with your favourite coffee mix at home, pack it into a tumbler and have it throughout the day. While it may be more troublesome, but you can save both money as well as the environment when you do so. Even better, if your office has a pantry with a coffee machine, you can get free coffee without having to do it yourself!

Trying to change your spending habits doesn’t mean forgoing your entire lifestyle completely. It can also mean looking at different alternatives and trying to find ways to get the biggest bang for your buck.

- Impulse purchases

According to Ryan Holmes, CEO of Hootsuite, we now see around 5,000 ads in a day. Whether we are in the train, or simply scrolling through our phones, we are constantly being tempted to purchase or subscribe to something.

If you have the habit of impulse shopping, then perhaps you should ask yourself these basic questions before purchasing.

- Do you already own something similar and has the same purpose?

- Will you regret it if you delay your purchase?

- Are there any cheaper alternatives to this item?

Otherwise, it would also be wise to sit on the intended purchase for a while. If it is something that you probably did not need, the impulse to purchase that item should go off. These questions can help you to re-assess if you really need the item, making sure that you are buying something that you really need. Once you break the habit of buying things that you may not have really needed in the first place, you’ll find yourself with more budget, and fewer things that might wind up gathering dust in your house.

- Using credit when you have cash

There are many pros when it comes to using a credit card. The card brings with it a lot of convenience as well as possible rewards. However, it can be very easy to overspend with a credit card. Just a tap here and a swipe there. Before you know it, your credit card bills can amount to a lot!

If you miss the payment cycle, you will be charged with a late payment fee. While you do not have to necessarily pay the full amount of your bill at the end of the month, paying just the minimum payment will still result in you having to pay interest which can be compounded daily.

Using credit cards may also encourage you to spend more money than you actually have, which can eventually lead to debt. So as much as possible, try to spend the money you have on hand so that you don’t end up spending more than your means.

- Spending without a plan

When you don’t have a set budget for the month, there is a higher chance of you spending unnecessarily. When you begin your planning, it is important for you to be aware of your needs and wants first. For example, if you are not saving as much as you would like because of your spending habits, then it is definitely time for you to take a step back and plan out what it is you truly need.

Before you spend on your wants, it is important that you spend on your needs first. This means spending on daily necessities such as food or rent. Another essential you should consider getting is personal insurance – starting from medical insurance – to provide coverage against unexpected large expenses when you fall ill.

After you have made sure that you are well-covered, you may also consider setting up different accounts where you can set budgets for different expenses, such as investments, food, transport, savings, etc. This will help to make sure you spend within your means and that you will have a minimum amount of savings every month.

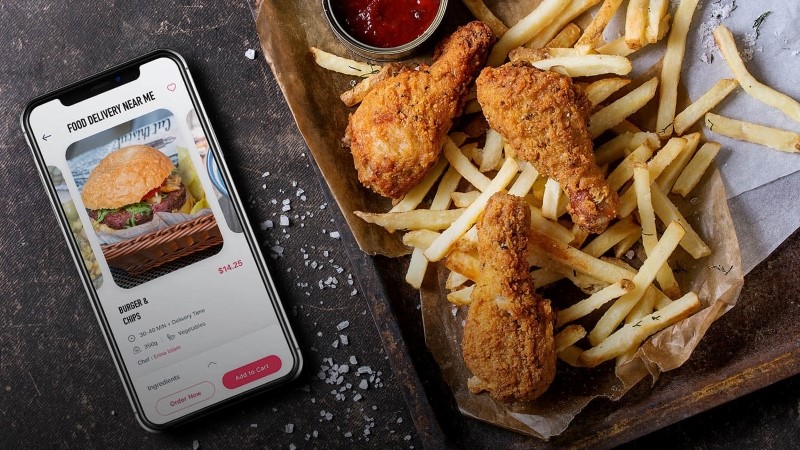

- Paying for convenience

Raining heavily, or just feeling lazy to head out? With a multitude of food delivery options out there, all we have to do is to lift a finger and we can get piping hot food delivered to our doorsteps. However, these can burn a hole in our wallet easily. With delivery fees as well as minimum order costs, it may not be a wise idea to continuously rely on food delivery.

Other conveniences that we commonly pay for include choosing to take a cab instead of public transport. While there are circumstances when we have no choice but to pay for these conveniences, constantly doing so will strain your budget.

If you are trying to save more money, choosing to take public transport over cabs, or buying food rather than calling for delivery whenever you can would help you to save a lot more.

Why is it important to save?

While these habits may not seem like a lot, they can amount to a lot in the long run. It is also important for you to practice healthy spending habits often, so that the same thinking can be applied to big-ticket items as well.

With better control over your spending, you will find yourself with higher disposable income. You’ll be able to invest and grow this extra amount of money instead of spending it all! A good plan you can consider starting with is an investment-linked plan or endowment plan. You could grow your money from as low as $100 a month. The best part is, these plans come with protection coverage in the case of death or terminal illness.

So, kick away those bad money-spending habits you have right now, and save your money for a rainy day!

Disclaimer:

This article is for general information only and does not take into account the specific investment objectives, financial situation or needs of any particular person. The views expressed herein do not necessarily reflect the views of AXA Insurance Pte Ltd and should not be construed as the provision of advice or making of any recommendation. There is no intention to distribute, or offer to sell, or solicit any offer to purchase any product. We recommend that you seek the advice of a qualified financial advisory professional before making any decision to purchase an insurance or investment product. Whilst we have taken reasonable care to ensure that all information provided was obtained from reliable sources and correct at time of publishing, information may become outdated and opinions may change. We are not liable for any loss that may result from the access or use of the information herein provided.

|

|

|

|